In an email sent on April 30th, CIMB Philippines announced that they will no longer offer the 4% p.a. interest for UpSave accounts and 4.1% p.a. interest for GSave accounts in the coming months.

Specifically, the standard interest rate will be lowered to 3% p.a. for UpSave accounts and 3.1% p.a. for GSave accounts starting June 1, 2020.

However, if one’s balance is at least Php 100,000 in June and July 2020, UpSave and GSave account holders can still earn an interest rate of 4% p.a. during those 2 months.

This is not surprising given the string of policy rate cuts by the BSP as of late in order to help cushion the blow from the current economic climate.

Aside from this, it is also possible that CIMB Philippines has built a good depositor base by now and no longer needs to offer interest rates that are significantly higher than other banks – although the revised rates are still higher than what other banks offer. Depositors of CIMB Philippines have also noted that the bank’s interest rates promotions have become less generous as of late, unlike the “double your monthly interest” promo late last year or the additional 1% p.a. interest rate between January to March this year. The most recent promo in April awarded an additional 0.5% p.a. interest rate only to selected depositors who got a text message announcement.

Where to place your CIMB PH funds after July 2020?

Even with the lower interest rates, CIMB PH still offers significantly higher than traditional banks. For comparison, savings accounts in BDO / Metrobank / BPI earn only 0.25% p.a. Within the sphere of digital banks, CIMB’s rates are still slightly higher than other banks so if you are the extremely conservative type who only puts money in a savings account, your funds will probably stay put with this bank.

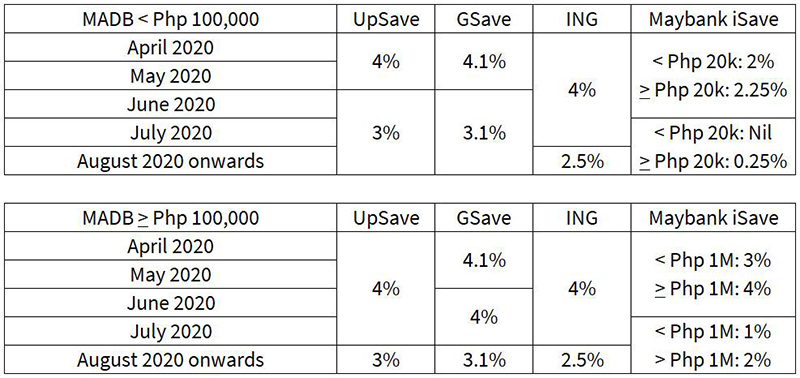

cimb ph revised interest rates compared with other banks

This table summarizes the interest rates in other digital banks between now and August 2020 when CIMB’s revised rates fully kicks in. As shown here, CIMB is still at least 0.5% p.a. higher than the nearest competitor, ING.

The revised interest rate of 3% p.a. is equal to the 1 year Philippine treasury bill yield of also 3% p.a. of this writing. Since the yield is the same, you can potentially put some in a government security which is generally perceived as safer, although the yield in a 1 year treasury bill isn’t compounding unlike a savings account where the interest is paid monthly. A 5 year government security currently yields 3.31% p.a. so depending on your horizon, a conservative investor can look at varying tenors of government securities as alternative to CIMB’s UpSave / GSave. The downside of placing directly in government securities is that it isn’t as liquid as a bank account. You can’t just pull out your debit card and withdraw cash from an ATM whenever you like. You can invest in government securities by buying directly in banks or by investing in similarly-themed UITFs.

As is also the tendency when interest rates fall, there is greater attention placed in other financial instruments with potentially higher returns such as stocks and that is also another thing to look into given the recent correction in prices.

You May Also Like

Graze at Hilton Kuala Lumpur – Wonderful Casual Dining in KL Sentral

Graze at Hilton Kuala Lumpur – Wonderful Casual Dining in KL Sentral- Coron, Palawan: Otherworldly Land & Seascapes

- Get Up to S$365 Worth of Bitcoin for American Express (AMEX) Credit Card Sign-ups

- My Singapore Airlines Business Class Experience (Singapore to Manila)

- CRU Steakhouse at Marriott Manila – An Instant Favorite

- Flight Review: Singapore Airlines Business Class on the Boeing 777-200 (Retrofitted)

Thanks for sharing this. At least I know I still have to keep my money at CIMB and ING to earn the high interest rates for June and July. By August, I will have to decide which bank I will keep my money at. Haha!